Wall Street Isn't To Blame For Knoxville's Housing Crisis

Despite attention from media and policymakers, institutional investors own less than 1% of Knox County's housing stock

Knox County Commission will soon consider a “Homes Not Hedge Funds” ordinance intended to ban institutional investors from purchasing single-family homes. This article, written prior to the announcement of the proposed ordinance, provides an overview of investor activity in Knox County’s housing market.

When Knoxville’s housing market exploded in the wake of the pandemic, institutional investors and corporate hedge funds became a popular scapegoat for the dramatic rise in local home prices. The argument is straight forward: Corporate investors, armed with algorithms and institutional capital, are buying up single-family homes at scale, outbidding ordinary families and driving prices out of reach.

It's a compelling narrative. But at least in Knoxville, it’s mostly wrong.

Data from Parcl Labs, a real estate analytics firm that tracks property ownership at the parcel level, shows that institutional investors own a negligible share of single-family housing in the Knoxville market. As of March 2026, investors of any kind—from small mom-and-pop landlords to larger, publicly-traded real estate investment trusts—owned roughly 8.0% of single-family homes in Knox County and 7.3% across the broader Knoxville metro area. Both figures have risen modestly over the past seven years, up from 6.5% and 5.7% respectively in January 2019.

To be sure, almost 1 in 10 homes owned by investors is not nothing. But the topline number doesn’t exactly tell the full story. Investor ownership, when broken down by portfolio size, provides much more insight into investors’ impact on the local housing market and, particularly, the rise in home prices.

For this analysis, investors are segmented into four tiers: small (2–9 properties), mid-size (10–99), large (100–999), and institutional (1,000 or more homes nationwide). Given hedge funds often operate through networks of obscure, rotating LLCs to obscure their ownership footprint, Parcl Labs data uses an algorithm that processes millions of data points across naming conventions, transaction patterns, corporate structures, and geospatial records to map LLCs back to their true corporate owners.

In Knox County, small-scale investors, often referred to as “mom-and-pop” landlords, account for roughly 75% all investor-owned properties. These owners are typically individuals or families who own a handful of rental homes—often as a supplemental source of income, retirement investment, or inherited property.

By contrast, large institutional investors own only 1.9% of all investor-owned properties. That equates to only 0.28% of Knox County’s single-family housing stock, or roughly 443 homes in a county with more than 214,000 total housing units, underscoring how limited the role of institutional investors actually is in the local market.

For every home in Knox County owned by Wall Street, small “mom-and-pop” landlords own roughly 38.

That begs an obvious question: are corporate investors who collectively own fewer than 450 homes—just 0.28% of the housing stock—really to blame for the broad-based rise in Knoxville home prices over the past five years? The honest answer is no.

Data on purchase-activity reinforces the point. A recent Realtor.com analysis, which utilizes a more expansive definition of institutional investors (i.e., any entity that purchased 350 or more homes from 2015 to 2025), found that institutional investors accounted for just 0.6% of all home purchases, or 1,428 total purchases, across the Knoxville metro area from 2015 to 2025. That figure is lower than most other competitor cities, such as Nashville (2.2%), Chattanooga (0.7%), and Greenville (1.2%).

In fact, among select U.S. metros in the Sun Belt, Knoxville had the lowest investor market share and the highest home price growth from 2015 to 2025—a direct contradiction of the prevailing narrative that institutional investors are driving the surge in prices.

In fact, the data points in the opposite direction: metros with the highest levels of investor activity, on average, experienced more modest price growth, while markets with relatively little institutional presence—like Knoxville—experienced some of the most rapid price appreciation.

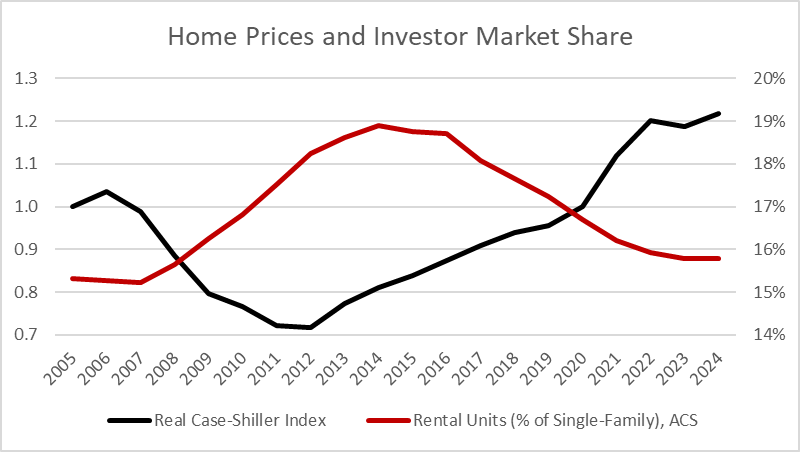

That doesn’t mean investors have no impact. But it does suggest they are not the primary force behind broad-based price increases. Data at the national level reinforces that point: Rental units as a percent of single-family homes—an (imperfect) proxy for investor market share—peaked in 2014 at 19%. But it has declined every year since, falling to a decade low of just under 16% in 2024. At the same time, house price growth surged even as the investor market share experienced a sustained decline, underscoring yet again that investor activity is only loosely connected to the broader trajectory of housing prices.

Taken together, the data points toward a much simpler explanation rooted in basic economics: strong population and household growth, driven by strong net migration, colliding with a housing market that has failed to build enough homes for well-over two decades. And the deleterious effects of that slowdown are visible over the long-run. From 1970 to 1980, Knox County’s housing supply expanded by 35%—prompting home prices to fall an inflation-adjusted 11% in the following decade. Since the 1970s, however, supply growth has slowed steadily, and real home price appreciation has climbed as a result.

Investors can, of course, intensify affordability pressures in certain neighborhoods, especially when purchase activity is highly concentrated. But that is a localized phenomenon, not the engine driving the broader housing market. The sustained upward pressure on prices is primarily the result of too many people competing for too few homes—a problem that no amount of investor regulation resolves without also addressing supply side constraints.

Investor Activity Concentrated in Handful of Large Metros

Institutional investors make up only a tiny fraction of single-family home purchases nationally, and their buying activity has been trending downward since peaking in 2021. Moreover, investor activity is highly concentrated geographically. According to Realtor.com, the top 10 metros by total activity account for over 50% of institutional investor purchases and the top 25 metros account for 75%—and Knoxville doesn’t make either list.

Even in metros with comparatively high levels of investor activity, institutional buyers still make up only a small share of overall single-family purchases. In Memphis—the leading metro by investor purchase share—they accounted for just 4.4% of total single-family home purchases from 2015 to 2025.

There is also substantial variation in within metros. Across Knoxville, only a handful of zip codes have an above average share of its housing stock owned by investors. Not surprisingly, neighborhoods near the University of Tennessee and the downtown core have the highest concentrations. The Fort Sanders area, which almost exclusively caters to UT students, stands out with investors of any size owning just over 22% of the total housing stock.

The downtown core, where around 13% to 16% of housing units are owned by investors, is also a magnet, largely driven by local short-term rental operators and other small-scale investors. By contrast, more suburban areas across Knox County tend to have a smaller share of their housing stock owned by investors, and an even smaller share owned by large corporate types.

Profile of Investor Purchases: Fixer-Uppers & Build-To-Rent

The are other reasons to question the “institutional investors are the problem” narrative, too.

Investors writ large tend to acquire lower value homes, oftentimes in need of significant repairs. According to Parcl Labs data, the median purchase price of investor acquisitions (existing-homes only) was just under $210,000 from 2019 to 2022—significantly below the overall median sale price. An analysis by East Tennessee Realtors from 2022, which uses a different methodology, similarly found that 46% of investor purchases in Knox County were for properties valued at $200,000 or less, with a quarter of all investor purchases priced below $117,250.

For the most part, these are not the move-in-ready homes that first-time buyers compete for at list price. They are, disproportionately, distressed properties: homes that need significant repair and are often not accessible for cash-strapped buyers. Without investor capital, many of these properties would sit vacant or deteriorate further. In this case, investors absorb the rehabilitation risk that neither individual buyers nor public programs are well-positioned to take on—and in doing so, return blighted or functionally obsolete units to the active housing stock. The result is an expansion of critical single-family rental supply that caters to households that cannot yet access ownership, such as working families and young professionals who need time and stability before they can save for a down payment.

Beyond existing-home purchases, nearly 1 in 4 investor purchases from 2019 to 2022 were for new construction, colloquially known as build-to-rent, at a median price of $521,000. These homes were never competing with ordinary buyers to begin with. They represent net additions to the housing stock, purpose-built for renters who either cannot or have not yet chosen to own.

To be clear, neither scenario is meant to suggest that all investor activity is a net benefit. Poorly managed rentals, speculative flipping without rehabilitation, and concentrated ownership in vulnerable neighborhoods can all cause real harm. The argument here is narrower: that the category of ‘investor’ is too broad to be analytically useful, and that policy responses calibrated to the Wall Street landlord problem will largely miss the actual market dynamics at work in Knoxville—while potentially discouraging the kind of small-scale investment that is doing some of the market’s most unglamorous but important work.

Why the “Investor Myth” Matters

Numerous studies have concluded that institutional investors are not to blame for the broad-based decline in housing affordability. That conclusion holds especially in mid-sized markets like Knoxville where their footprint is negligible. Yet the narrative persists—animating residents, commanding headlines, and shaping local policy conversations that should be focused elsewhere.

That misdirection has a cost. When the political energy around housing affordability concentrates on Wall Street landlords and institutional buyers, it crowds out more important conversations about zoning reform, permitting, and the mismatch between the homes the market needs and the homes the regulatory environment allows builders to produce profitably.

Knoxville is not a market where policy restricting institutional investor purchases will meaningfully change affordability. Institutional investors own fewer than 500 homes and, even if every one of those homes were returned to the for-sale market tomorrow, it would represent a rounding error against the county’s housing deficit.

The Knoxville housing crisis is real. Its causes are structural: too little available housing supply, too much demand, and a construction sector limited by scarce labor and zoning policy that starkly limits how much housing can be built and where. Fixing it requires confronting those causes directly. That work is harder and less satisfying than blaming a hedge fund—but it is the only thing that will move the needle on housing affordability.

My Position On the “Homes Not Hedge Funds” Ordinance

For many of the reasons outlined above, I do not support an ordinance banning institutional investors from purchasing single-family homes in Knox County. The ordinance makes it unlawful “for any person, including any affiliate of such person, to purchase more than one hundred (100) single-family homes within Knox County if such purchases are made primarily for rental purposes,” applicable to all purchase contracts entered into on or after the effective date of the Ordinance.

As currently written, the proposed ordinance is vague, will be exceedingly hard to enforce, and require significant county staff time and resources—while producing no measurable improvement in affordability. That said, I’m not particularly passionate about the issue as institutional investor activity is very limited in Knox County and, therefore, the ordinance would have little practical impact on the market.

However, if the proposed ordinance moves forward, policymakers should consider making the following clarifications and/or amendments:

Add Defined Time Horizon: The current language prohibits purchasing more than 100 single-family homes with no temporal limit, meaning the restriction accumulates indefinitely from the effective date. Without a defined time horizon, a local remodeling company that acquires and rehabilitates distressed properties before renting them—returning vacant homes to productive use—could run afoul of this provision over time despite providing clear community benefit. The language could be amended to read: “It shall be unlawful for any person, including any affiliate of such person, to purchase more than one hundred (100) single-family homes within Knox County in any five year period if such purchases are made primarily for rental purposes.”

Exempt Build-To-Rent (BTR) and New Construction: The current language does not provide any exceptions for build-to-rent communities. BTR adds new housing supply rather than competing for existing homes and should therefore be exempted, as effectively banning BTR would only serve to further constrain housing supply. Moreover, BTR’s unique financing structure—backed by large capital sources, rather than smaller bespoke home builders—can allow renter access to a single-family home in areas that might otherwise be unaffordable. Given that BTR communities are functionally indistinguishable from conventional multifamily development—differing only in unit type—there is no coherent policy rationale for treating them differently. New construction and BTR should be explicitly exempted.

Expand Rental Purpose Window: The ordinance current defines rental purpose as “the intent, at the time of purchase or within twelve (12) months following purchase, to lease or rent the property to one or more tenants for residential occupancy in exchange for compensation.” When investors or home remodelers acquire distressed properties for rehabilitation, they often need to rent the property for at least 3-5 years to recoup costs before ultimately reselling the property. The current 12- month window is too narrow and could impede home rehabilitation efforts, which bolster housing supply in the long-run.

Recommended Further Reading:

Will Regulating Large Institutional Investors Actually Make Housing More Affordable? — Urban Institute

Institutional Investors in the US Housing Market: Myths and Realities — AEI Housing Center

The Shrinking Institutional Investor Footprint: National Trends and Local Concentration — Realtor.com

How Many Homes Do Corporate Landlords Really Own? — The New York Times

Institutional Investment in Single-Family Housing: Separating Fact from Fiction — Progressive Policy Institute

This is an excellent piece of policy analysis, fairly done. I am no expert in housing policy but I know a great deal about policy analysis, and I convinced by your analysis.