Knoxville Home Prices Post First Decline Since 2012

Home prices declined 1.4% year-over-year in the final quarter of 2025. But the drop has already been wiped out.

A note from me: Thank you for reading and supporting my work. I write these articles as a free public resource to help citizens, real estate professionals, and policymakers better understand East Tennessee’s housing market and how it impacts the people’s everyday lives.

The research, data analysis, and visualizations behind these pieces take a significant amount of time to produce. If you find this work valuable, I’d be deeply grateful if you shared these articles with others and encouraged those who care about housing, growth, and public policy in East Tennessee to subscribe as well. Your support helps make this work possible.

Home prices across the Knoxville metro declined in the fourth quarter of 2025, falling 1.4%—or 3.6% in inflation-adjusted terms—from the prior year. It marks the first year-over-year drop since 2012, snapping a streak of uninterrupted appreciation that survived the pandemic, a doubling of mortgage rates, and one of the most aggressive Federal Reserve tightening cycles in recent history.

The decline, however, was short-lived. By the first quarter of 2026, Knoxville home prices rebounded, rising 4.5% year over year—or 1.9% after adjusting for inflation. Even so, the brief downturn was a notable inflection point for a market that has seen home prices more than double since 2019.

Home price growth in Knoxville is nonetheless expected to slow across 2026. A sustained decline or broad-based price correction still remains highly unlikely—the structural demand drivers that fueled the dramatic rise in prices remain intact, albeit much less pronounced.

Affordability constraints, driven in large part by elevated mortgage rates, continue to keep a significant share of would-be buyers on the sidelines. But underlying demand-side factors—continued in-migration, low unemployment, changes in household composition, and relatively low inventory levels—should provide enough of a floor to prevent outright price declines. Accordingly, I expect Knoxville home prices to increase modestly in 2026—roughly 1% to 3% annually—with real, inflation-adjusted price growth likely flat to slightly negative.

That forecast, however, is more uncertain than usual and depends on a multitude of extraneous factors. Mortgage rates remain the single most influential factor: rates rose to the highest level since the summer of 2025 in recent weeks, according to Freddie Mac. The impact of rates is hard to overstate: for example, a one percentage point decrease in rates would allow more than 14,000 additional households across Knoxville to afford the median-priced home—assuming they can cover the down payment.

Yet, most forecasters and housing market analysts—myself included—do not expect mortgage rates to meaningfully decline in 2026, as inflation remains well above the Federal Reserve’s 2% target. Fannie Mae’s latest forecast projects 30-year FRMs to average 6.3% across 2026 and 6.2% in 2027. Especially with the recent uptick in inflation—which rose to a three-year high in April—rates are unlikely to fall enough to bring prospective buyers off the sidelines. Conversely, if mortgage rates continue to climb and surpass 7.5%—which is also not likely at this point—home prices are almost certain to fall.

Geopolitical risks also introduce uncertainty. The ongoing war in Iran has pushed oil prices and inflation expectations higher, as evidenced by the recent run up in treasury yields. While recent reports of a potential agreement to end the conflict offered some encouragement, the U.S. this week launched additional strikes on Iranian military assets, further complicating already fragile negotiations over the fate of the Strait of Hormuz and the prospects for a lasting ceasefire. All things considered, there’s little indication the conflict will be resolved quickly—making a sustained decline in either inflation or mortgage rates this year less likely.

Ultimately, the range of plausible outcomes in 2026 is much wider than it has been in years. That is itself a trend worth paying attention to.

Affordability Constraints Holding Back Home Sales

Affordability remains the primary impediment for most homebuyers.

As of May 2026, a family earning $75,000 per year could afford just under 13% of homes listed for sale with a 5% down payment. That figure rises to 25% of homes with a 20% down payment. Importantly, these estimates do not include households that make more than $75,000 but who cannot afford the required down payment.

In a balanced market, where the price distribution of listings is generally aligned with the income distribution of households, annual income of $75,000 should be enough to afford roughly half of homes.

Rent Growth Slowing, But Typical Rents Are Still Over 50% Higher Than 2020

The rental market—which tends to respond more quickly to new supply and broader economic conditions than the for-sale housing market—continues to experience a pronounced slowdown in both rent growth and demand.

Single-family rents have been relatively stable since mid-2025, with annual rent growth generally hovering between 1% and 3%—below pre-pandemic norms and dramatically lower than the more than 20% growth recorded at the height of the pandemic-era housing boom in 2022. Since the beginning of 2024, the typical single-family renter has seen their rent increase by just under $150 per month.

By contrast, the multi-family market has experienced considerably more volatility—largely due to the historic numbers of new units that started construction in the early pandemic years and are now coming online. Annual multi-family rent growth has been mostly negative since November 2025 and since the beginning of 2024, the typical apartment renter has seen their rent increase by roughly $50 per month.

With a significant amount of new supply expected to become available over the next 12 months, multi-family rents will likely further soften in 2026—and could end the year in negative territory. But those declines, if they materialize, are unlikely to translate into rent cuts for existing tenants. More likely, many current renters will simply be offered lease renewals with little or no increase, while the bulk of concessions and pricing reductions will be concentrated in new leases.

Even though most leading indicators point to a softening rental market in 2026, there is still some some upside potential. Knoxville’s apartment vacancy rate currently sits at 6.6%—well below the 8.0% in Tennessee and 7.2% nationwide—according to Apartment List data. Generally, a vacancy rate of ~7-8% is considered a healthy or balanced market, where there is enough availability for renters to have options and more negotiating power, but not so much that units become hard to fill without sizable concessions.

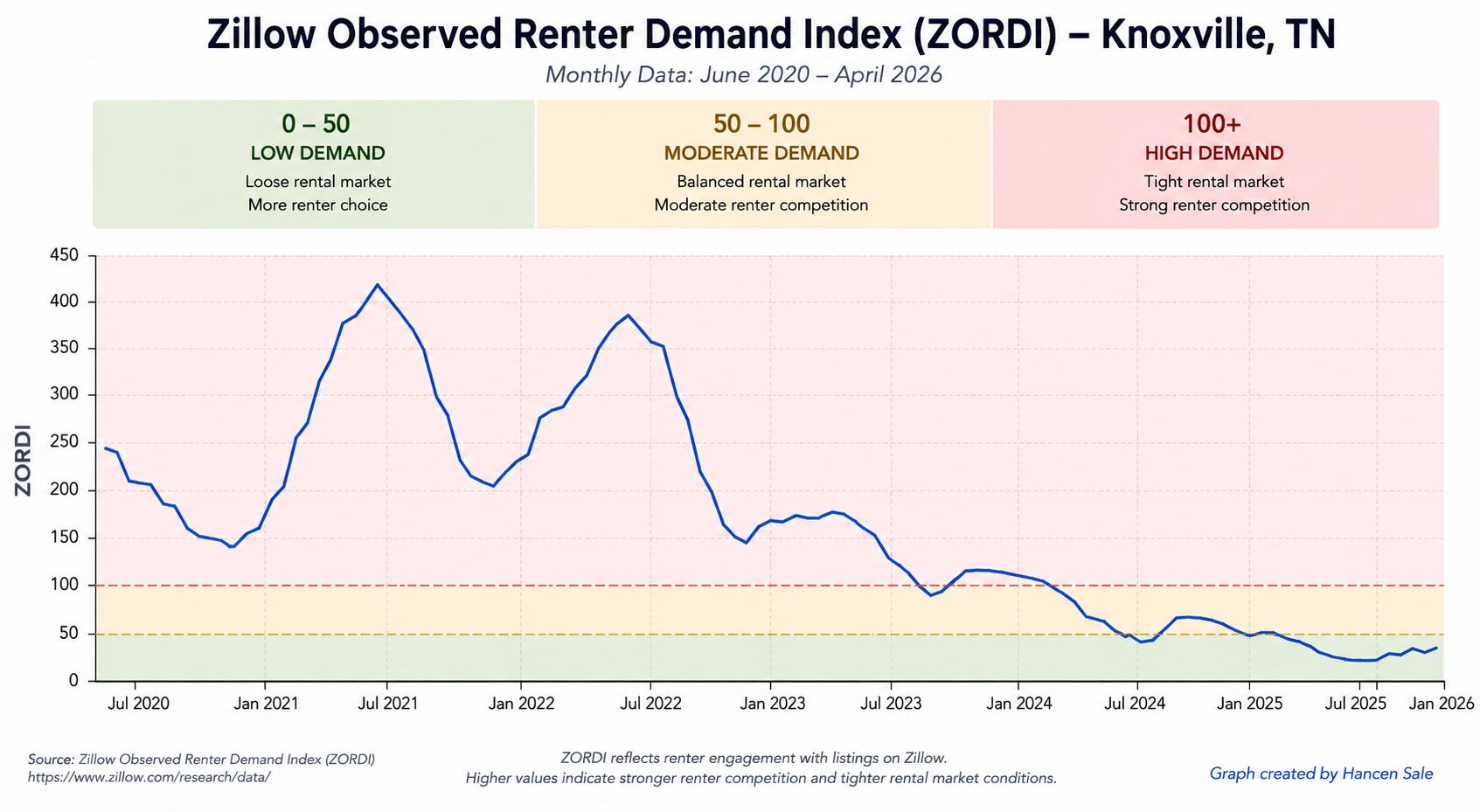

In addition to “hard” data points like rent growth or vacancy rates, forward-looking private sector data also points to a softening market. Zillow’s Observed Renter Demand Index (ZORDI), which tracks the number of individuals actively searching for rental listings, helps to visualize the dramatic reversal Knoxville’s rental market has undergone since the pandemic-era housing boom.

ZORDI measures renter competition and overall rental market tightness based on renter engagement with listings on Zillow. Higher values indicate a tighter, more competitive rental market, while lower values suggest softer conditions with more renter choice and slower rent growth.

The index peaked above 400 in 2021 and 2022, reflecting an extremely competitive rental market. Since then, renter demand has declined considerably. By 2024 and 2025, however, the index had fallen sharply into the “low demand” range, suggesting a much softer rental market with slower rent growth, more renter bargaining power, and increased supply availability.

The trend reflects a combination of easing migration demand, affordability constraints, and—most importantly—a substantial increase in multifamily housing supply across the Knoxville region. While demand remains healthy in absolute terms, supply growth has begun to ameliorate the severe supply-demand imbalance.

The single-family rental market, however, is in a comparatively stronger position. Unlike the apartment sector, where thousands of new units have recently hit the market, the supply of single-family rentals has expanded much more gradually, meaning there is a firmer floor under single-family rent growth even as overall rental demand cools.

Last Thoughts

At a broad level, Knoxville’s housing market remains fairly strong. As has been the case for several years now, the frenetic conditions that defined the pandemic-era boom are decidedly gone and aren’t likely to return in the near future. The market is gradually rebalancing, particularly on the rental side, where new supply has finally begun to ease some of the pressure that built up over the last several years.

That said, “normalizing” should not be confused with “affordable.” Even with slower home price and rent growth, affordability remains deeply strained for many households—largely because prices and rents rose so dramatically in such a short period of time.